Global Economic Outlook: Diverging trajectories of growth and interest rates

Vice President, Economist

- Global growth is expected to remain fragmented, with the US and emerging markets seeing strong growth momentum through 2024, while the EU and the UK remain lacklustre for the year.

- Switzerland initiated the first interest rate cut among advanced markets in March 2024, paving the way for the global rate cut cycle to continue, likely led by European economies.

- Japan exited negative interest rates in a landmark decision in March, but more signs are needed to confirm an exit from its deflationary mindset. Lingering negative real wage growth means that the uplift in growth for Japan is not yet well-sustained.

- In South and Southeast Asia, there are increasing signs that domestic consumption and investment are taking hold as key growth drivers, while the outlook for the more export-oriented economies has turned uncertain amid slower global trade flows.

After decelerating rapidly in 2023, headline inflation is getting more sticky and the path to converge with central bank targets of around 2% inflation rate is proving more difficult than anticipated. Core inflation is hovering at relatively high levels and, in some economies, has even nudged up slightly in the early months of 2024. The pick-up in inflation reflects strong wage growth and core services inflation, although prices have also been affected by seasonal distortions as well as a rise in maritime freight rates due to the conflict in the Middle East. Central banks remain cautious about the pace of inflation decline towards their targets and are likely to only start cutting interest rates in the latter half of 2024.

Diverging growth outlook: The US and emerging markets are showing strong momentum. The US economy, particularly its consumer segment, continues to defy expectations of a slowdown this year. Despite high US interest rates and tightening credit and bank lending standards, consumer spending has remained resilient, underpinned by strong labour markets (Figure 1). Consumer spending, which accounts for two-thirds of economic activity in the US, grew at 3.0% annualised in 4Q2023 alongside business investment growth of 2.4%. Meanwhile, real personal income posted a robust 3.2% annual growth, carrying a strong momentum into 2024. Jobless claims remain close to their all-time lows, signifying the strength of the labour markets in the US. That being said, we expect the impact of high interest rates to eventually weigh on the labour markets, cool consumer spending and squeeze corporate margins, opening room for the Fed to cautiously cut interest rates in the second half of 2024.

Figure 1: US wage growth and inflation have moderated, but remain at high levels

Source: Bloomberg, US Atlanta Fed

Modest growth outlook for Europe and the UK

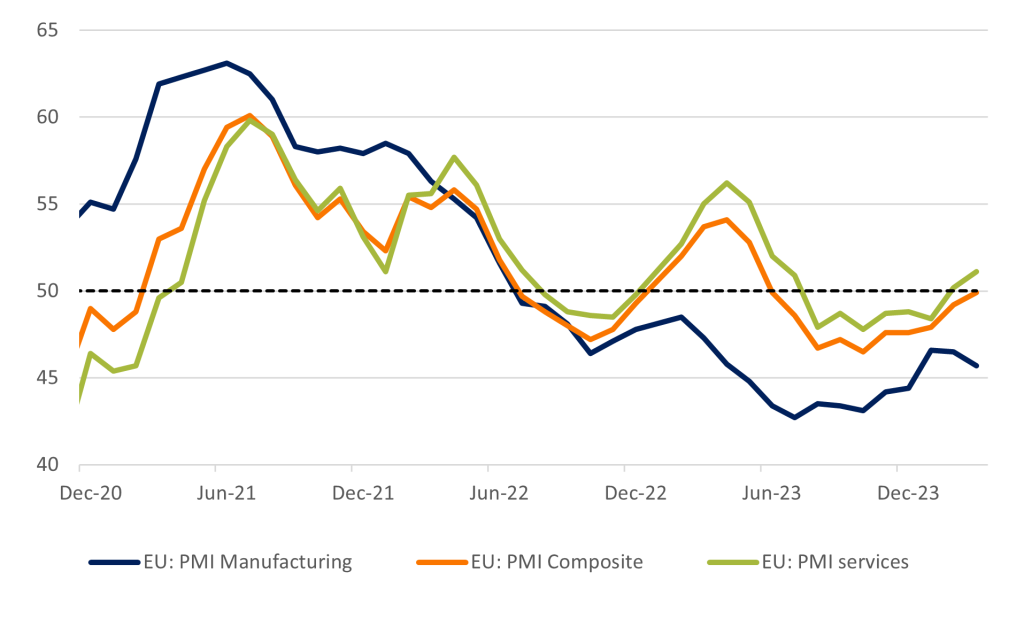

In Europe and the UK, growth has stagnated over the past few quarters, characterised by a protracted cost-of-living crisis and high interest rates bearing down on consumers and businesses alike. More worryingly, the manufacturing sector in the EU, particularly in Germany, has remained in contraction since 2022, not having recovered from the energy shocks following the Russia-Ukraine crisis and further depressed by high financing costs and labour shortages. The services sector, on the other hand, is beginning to show green shoots (Figure 2) as real wages ticked higher in both Europe and the UK over the past year.

We expect only modest growth for Europe and the UK in 2024, given the lack of strong positive momentum drivers on the horizon. Consumer confidence has troughed but remains weak. On the external front, the global trade outlook has remained lacklustre in part impacted by geopolitical tensions and rising protectionism. The European Commission and the UK government both project their market’s GDP growth to trend at 0.8% in 2024. There is also heightened uncertainty around the impact on inflation from rising geopolitical tensions in the Red Sea, as maritime fares rise sharply and the global supply chain is again disrupted. An escalation in tensions in the Middle East and resulting disruptions to supply chains may further weigh on business and consumer confidence in this region .

Figure 2: EU PMIs point to an anaemic manufacturing sector but a recovery in services

Source: Trading Economics

Switzerland kicked off the global rate cut cycle

Switzerland became the first advanced economy to cut interest rates in March 2024. While there are no imminent recession risks for the economy, growth has weakened. More crucially, Swiss inflation has consistently stayed below the Swiss National Bank (SNB)’s inflation target of 2% since July 2023 and declined to 1.2% in February this year. This marked the end of a prolonged period of high inflation exacerbated by COVID-related supply chain disruptions and high energy prices from the fallout of the Russia-Ukraine war. The SNB forecasts inflation at 1.4% for 2024 and growth of around 1%, suggesting that both macro-indicators are supportive of a monetary adjustment. While this indicates the SNB’s confidence in achieving price stability while avoiding a recession, other central banks may take longer to embark on the cutting cycle as inflation in most other advanced markets still hovers around 4%.

Japan exits negative interest rates, but can it shake off ultra-loose monetary policy?

The Bank of Japan (BoJ) raised its interest rates for the first time in 17 years this March, ending eight years of negative interest rates for the Japanese economy. The Bank assessed its price stability target to have been achieved sustainably, following the annual spring wage negotiations where a historic wage hike of 3.6% was deemed to trigger a virtuous cycle between wages and prices (Figure 3). BoJ also reduced its quantitative and qualitative easing (QQE ) by discontinuing purchases of ETFs and J-REITs and announcing a gradual reduction in purchases of CPs and corporate bonds over the year, while still maintaining JGB purchases.[1]

While this decision is seen as momentous for Japan, it is uncertain whether the economy can swiftly overcome nearly two decades of a deflationary mindset that has taken hold among domestic corporations and consumers alike. While progress has been observed in nominal growth of wages and inflation, several structural issues behind Japan’s secular stagnation remain unaddressed, and indeed, outside of the control of monetary policy. For instance, Japan’s ageing demographic is a significant driver behind shrinking demand and investments. This is illustrated in personal and household consumption growth having remained lacklustre despite the hike in nominal wages over the last two years. In fact, weak personal consumption has been pulling down growth, with Japan only narrowly skirting a technical recession in the second half of 2023 (defined as two consecutive quarters of negative growth).

Figure 3: Wage hikes and real wage growth in Japan

Source: CEIC, Japan Labour Issues, vol. 8, no. 46, Winter 2024

Lessons from an era of negative interest rates

The effectiveness of aggressive monetary easing and ultra-low/negative interest rates in achieving inflation targets is a topic of ongoing debate. Arguably, the global rise in prices over the past couple of years was largely influenced by exogenous factors, such as supply chain disruptions and firmer oil prices, that led to higher cost-push inflation.

An earlier paper from the European Parliament estimated that negative interest rates added about 0.7 percentage points to loan growth each year and argued in a counterfactual exercise, that inflation and real GDP would likely have been much lower in the absence of non-standard measures such as the negative interest rate policy (NIRP).[1] However, the price of credit was likely not the key determinant for the sluggish growth in the EU . Factors such as declining competitiveness and slowing global trade have also been weighing on the region’s growth.

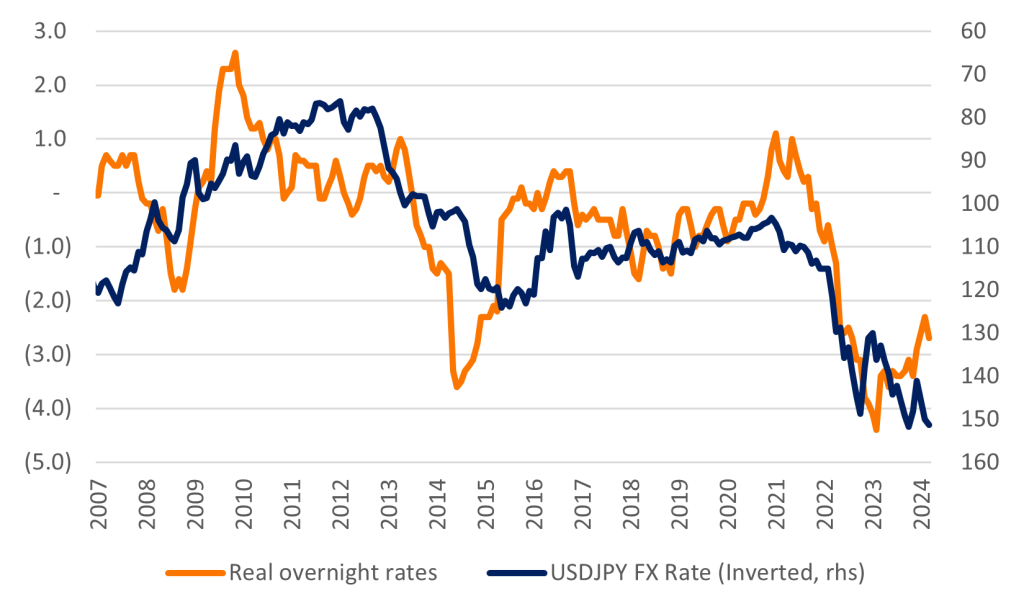

Similarly, interest rates in Japan have been close to zero or below zero since 1997, but ultimately the triggers that drove up inflation in Japan were largely external, including supply chain disruptions and higher global oil prices. With inflation rising higher due to exogenous factors, a highly negative real rate differential against other currencies supported further yen depreciation (Figure 4). The weaker yen provided a boost to exports and corporate profits, while also adding to imported inflation.

Figure 4: Decline in Japan’s real interest rates in mid-2022 drove JPY weakness

Source: Bloomberg

The combination of negative interest rates and quantitative easing policies also distorted asset prices. Over the past decade, the global financial system was flush with trillions of dollars of excess liquidity (Figure 5), creating pockets of exuberance in some asset markets. Negative interest rates also weighed on bank margins, as excess reserves were penalised while banks often found it difficult to pass on the negative interest rates to savers. However, experience showed that ultra-loose monetary policies also promoted risk-taking by banks, and the positive impact on banks’ assets (due to global excess liquidity and market exuberance) could partly compensate the negative effects from lower interest rate margins.

Figure 5: Global central bank balance sheets since 2007

Source: Bloomberg, central banks

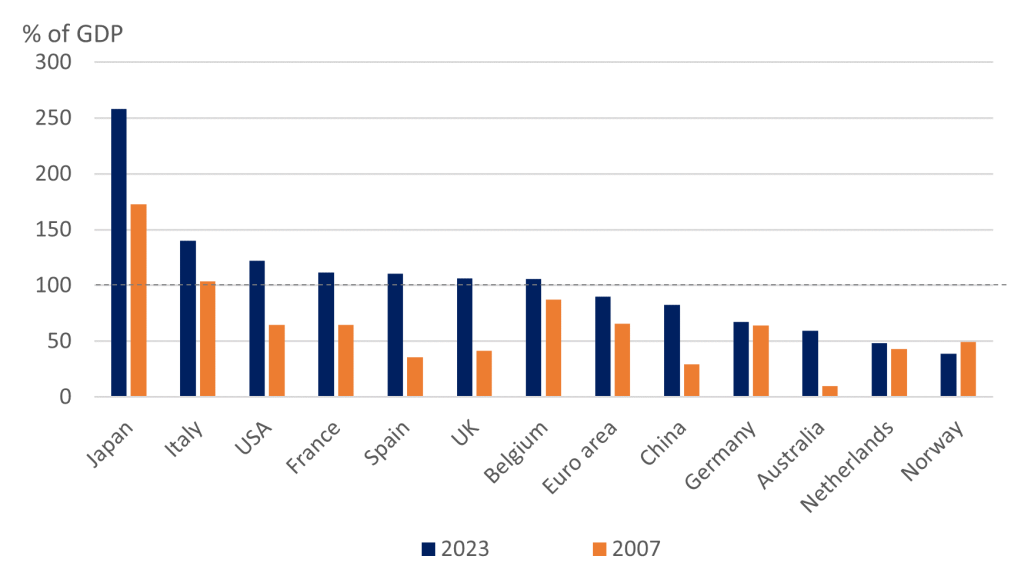

More worryingly, the ultra-loose monetary policies played a role in expanding fiscal deficits in advanced markets. Governments have amassed record levels of debt over the past decade, partly enabled by central banks that bought large volume of government bonds at low rates, as part of quantitative easing targets (Figure 6). As central banks dial back QE and raise the cost of borrowing, there are increasing pressures on fiscal balance sheets and in turn on overall economic growth. A lack of a credible plan to consolidate debt could also affect investor confidence and credit ratings, a key concern in a shrinking AAA debt world.

Figure 6: Government debt has grown significantly since 2007 in many advanced markets

Source: IMF

Emerging markets are increasingly a major engine for global growth

Emerging markets’ growth has held up well over the past couple of years despite an uneven distribution across different markets. The outlook for emerging markets this year is likely to remain positive, as advanced markets are expected to avoid a recession and financial conditions are set to ease in the second half of the year.

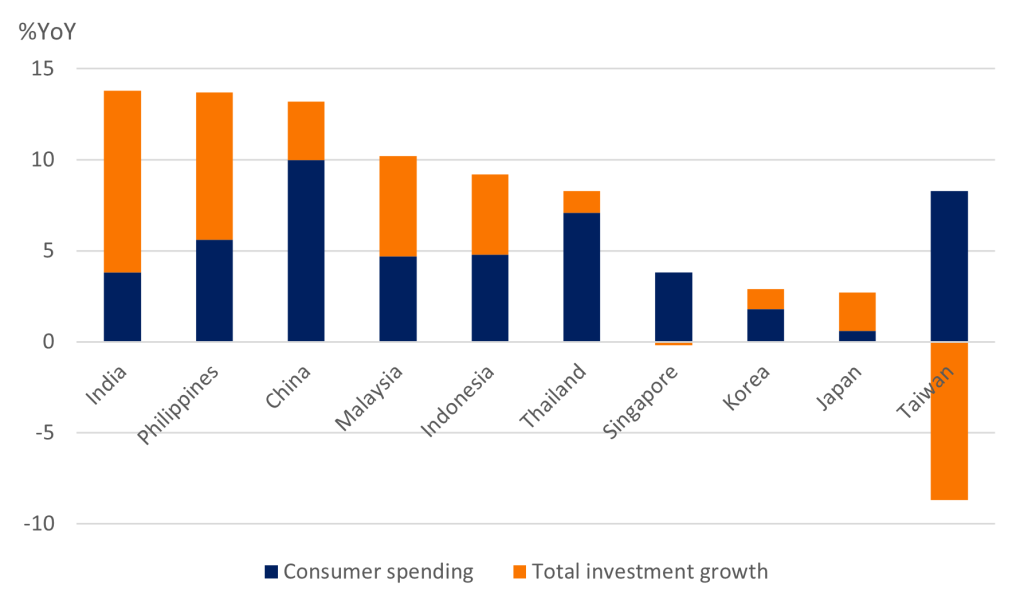

Within the emerging market universe, Emerging Asia (ex-China) stands out in terms of the increasing strength of the domestic economy and a lower reliance on external demand, particularly in South and Southeast Asia (Figure 7). These regions are witnessing a significant change in consumer habits fueled by economic growth and optimism about the future among its large young middle-class population. Digitalisation and an increase in internet penetration in the past few years have provided another impetus to the spending and investment habits of the youth, in addition to creating new business and job opportunities for this demographic segment.

Figure 7: Domestic consumption and investment growth across Asian economies

Source: CEIC

Looking across Asia, India and the Philippines are leading the region in terms of real growth, while Singapore, Korea and Taiwan (the more developed and export-oriented markets) are lagging. Private consumption spending has been resilient for much of the region, amid stable labour markets. Unemployment rates are below pre-pandemic levels in most markets, except Indonesia, Thailand and China. In Thailand and Indonesia, private spending has also been backed by a tourism recovery, which is helping to support household incomes in these economies.

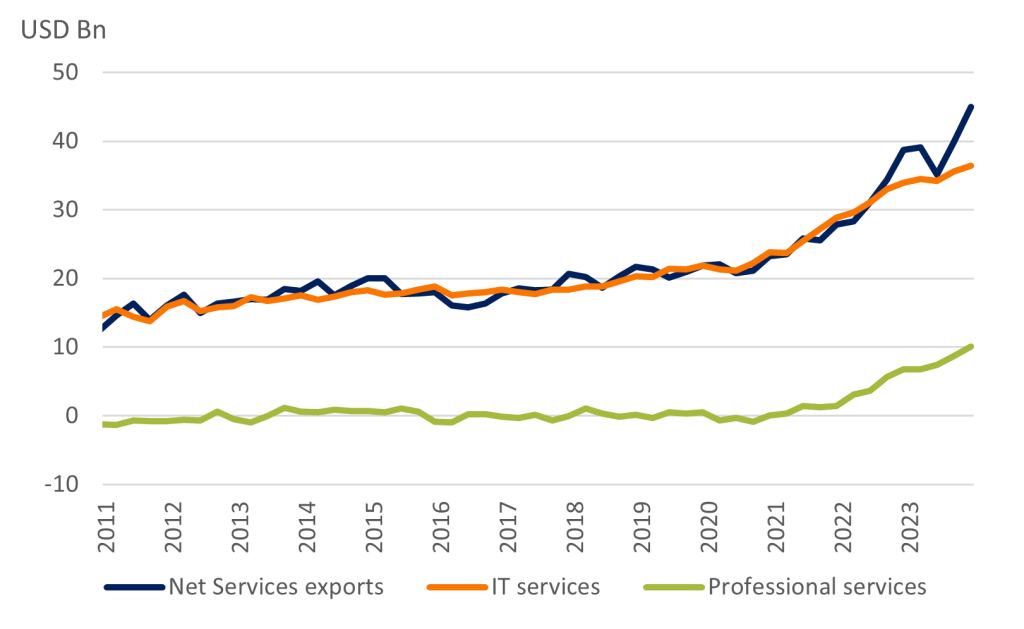

Robust growth in India and the Philippines is underpinned by increasing public investment, in addition to resilient private consumption. For both economies, the central government’s bid to improve infrastructure has been a significant driver for capital expenditure. In India, private investments in real estate are also rising, supporting construction, and housing sectors. Consumption in both economies benefits from the strength of their services exports (Figure 8) and a vibrant informal sector that is increasingly being tapped by the tech-savvy youth. The medium-term outlook remains bright. In particular, there is sustained high interest to relocate manufacturing to India, particularly in the tech industry, while the country’s share of global exports is also rising steadily.

Figure 8: India services exports are strengthening beyond IT services (net exports, quarterly data)

Source: CEIC, Reserve Bank of India

Uncertain economic outlook in China. Pressures on China’s economic growth persist from its faltering property market and ongoing geopolitical tensions with advanced markets. That said, early in 2024, some economic activity indicators are showing signs of stabilisation. China’s Purchasing Manufacturing Index (PMI) moved into expansion territory and industrial output showed an improvement to 7% year-on-year growth for the period of Jan-Feb this year. Services activity also showed resilience during the Chinese New Year holidays.

The property sector, however, remains weak. Property investment dropped -9% year-on-year in January-February 2024, and land sales revenue indicators were flat. A number of supportive policies have been issued since late 2023 such as improving financing availability for developers, lowering mortgage rates for first home purchases and providing tax incentives to home buyers. Beyond these measures, fiscal policy support is focused on infrastructure investment. It remains to be seen if these measures would be sufficient to stabilise the property markets, as well as providing an uplift to the subdued consumer and business sentiment in China.

Summary

The global economic outlook is fragmented, with the US and emerging markets showing better-than-expected resilience in growth. On the other hand, in the EU and the UK, growth has stagnated in recent quarters and the outlook remains modest, at best. As a result, European countries are likely to lead the global interest rate-cutting cycle this year, with Switzerland having already delivered its first rate cut in March. Within emerging markets, we note a rising trend of domestic growth drivers particularly in South and Southeast Asia, that are adding to the resilience in demand from emerging Asia. Finally, in Japan, we discuss the end of the negative interest rate policy and its implications. We believe that multiple structural causes of deflation in Japan are likely unaffected by the change in monetary policy. As such, there is a need for sustained rise in real (not only nominal) wages, before consumption demand stabilises and allows for a sustainable price-wage cycle.

[1] Bank of Japan: Changes in the Monetary Policy Framework, 19 March 2024

[2] European Parliament: What Are the Effects of the ECB’s Negative Interest Rate Policy?, Monetary Dialogue Papers, June 2021

Other Insights

Wed, 22 Apr 2026

| 16 mins

|

Frankie Chan

Tue, 24 Mar 2026

| 19 mins

|

Kritika Kashyap

Fri, 30 Jan 2026

| 18 mins

|

Kritika Kashyap

Mon, 27 Oct 2025

| 10 mins

|

Kritika Kashyap

Elevate Your Business

with Peak Re

with Peak Re