How Urbanisation, Digitalisation, and the Gig Economy Are Redefining Needs of the Emerging Asian Middle-Class

Vice President, Economist

Senior Vice President, Market Research and Insurance Analyst

Summary

- Rapid urbanisation and digital transformation of Asia’s emerging middle class are reshaping consumption patterns, risk profiles, and insurance needs. This article highlights six key trends to watch.

- The rise of the gig economy and lifestyle shifts towards service and sharing models are increasing demand for insurance flexibility, income protection, and personal cyber risk coverage.

- Understanding these shifts offers insurers an opportunity to capture growth by tailoring innovative, digitally enabled insurance solutions that resonate with this high-potential demographic.

Introduction

The burgeoning middle class in Emerging Asia is one of the defining economic forces of recent decades. More than half of the world’s population now belongs to or above the middle-class segment[1], with Asia housing 60% of this demographic.[2] This segment is projected to generate 60% of new global consumer spending in this decade (between 2021 and 2030) – the equivalent of adding a second United States to the global economy.[3]

This article highlights some of the key trends that will shape the outlook of the middle class, particularly in Emerging Asia. Urbanisation, evolving consumption, and digitalisation are expected to shape this market’s financial needs and risks, which insurers must understand to seize growth opportunities.

Urbanisation and Consumption Trends

A strong positive correlation is observed between economic development and urbanisation. Urban areas offer more diverse and higher-paying jobs, better education, and more entrepreneurial opportunities, thereby enabling more people to achieve middle-class status. According to the United Nations (UN), urban centres are responsible for more than 80% of the gross national product.[4]

Trend 1: Services over goods consumption

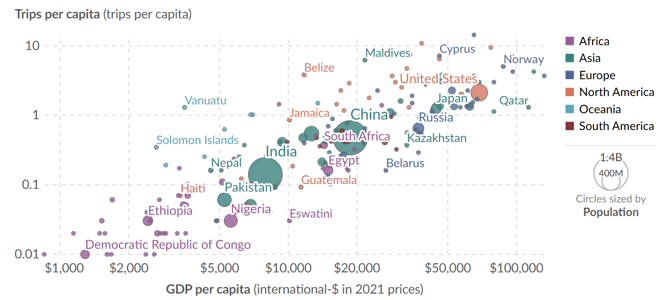

A typical feature of urbanisation is the higher marginal propensity of the middle-class to spend on services such as education, overseas travel, healthcare, and entertainment. While middle-class consumers also spend on better food and affordable luxury, rising income often means increased discretionary expenses, particularly on so-called “experiential spending”, such as on travel, attending events or gathering unique experiences. At the same time, services also account for an increasing proportion of middle-class employment. Figure 1 below shows the linear correlation between income and the number of air travel trips

Figure 1: Number of air travel trips vs. GDP per capita, 2019

Source: OurWorldinData.org/transport.

Data source: Airbus (2019); Eurostat, OECD, IMF, and World Bank (2025)

Note: GDP per capita is expressed in international-$ at 2021 prices.

Trend 2: Sharing over owning

Along with a shift towards spending on services, urbanisation and the rise of the middle-class also drive more demand for assets, such as properties, real estate and cars in these urban centres.

Affluent Asians have traditionally invested in properties for long-term investments. However, these are susceptible to risks of negative equity whenever economic growth slows and property prices drop. Owning properties also exposes the middle class to the impact of climate change through more frequent and severe weather events. In some markets, mortgages are the single largest financial liability of middle-class families, making term life insurance, or mortgage life insurance critical protection tools for families.

However, urbanisation, digitalisation and the rise of the subscription/sharing economy means that some in the middle class (particularly some in the younger generations) are preferring renting and sharing [5], as opposed to owning and buying (think housing-as-a-service and car-as-a-service instead of buying a home or a car), endorsing an “asset-light” lifestyle. Sometimes, this can be more cost-effective for consumers and offer more flexibility, such as swapping a sedan for an SUV for weekend trips.

As a result, consumers would also expect a similar experience and flexibility in related insurance products. For instance, usage-based-pricing for auto insurance, such as “pay-per-mile” or driving behaviour-based discounts, are likely to gain more traction with these trends.

Trend 3: Urban lifestyle’s impacts on physical and mental health

Urban living often leads to lifestyle changes that influence spending patterns. For example, middle-class consumers in cities typically spend more on dining out, travel, and leisure activities than their rural counterparts. Additionally, urban sedentary lifestyles can lead to a higher prevalence of certain chronic diseases, and environmental concerns like air pollution increase susceptibility to respiratory conditions.

The urban lifestyle has also been linked to mental health decline among urban dwellers, for instance, due to loneliness and stress.[6] On the other hand, cities have better access to care and a high health service utilisation rate,[7] which can help to mitigate the negative impact of chronic and mental issues.

A somewhat related, rising trend is of “time poverty”[8]. Despite material improvements, time poverty affects physical and emotional well-being, for instance, through working parents finding less time to care for their children or individuals spending too much time on digital devices. Implications can range from sleep deprivation to physical health decline, increase in loneliness and anxiety, and impact on productivity and focus. One possible value proposition of medical insurers is to help alleviate consumers' "time poverty", likely as part of healthcare advisory services.

Digital Transformation and Cybersecurity Risks

Asia is undergoing rapid digitalisation, impacting almost every aspect of middle-class consumers' daily lives. The digital trends have accelerated since the COVID-19 pandemic, and are changing how the middle-class consumes.

Trend 4: Digital-first consumption

E-commerce and Super Apps have flourished, and consumers are increasingly shifting from physical to online shopping. According to the World Economic Forum, the two fastest-growing e-commerce retail markets globally are the Philippines and Malaysia.[9]

- For fast-moving consumer goods (FMCG), supermarkets and virtual malls, both now have a similar market share of around 20% each [10]. On the other hand, for tech and durable goods, there is an increasing fusion of online and offline retail.[11] Retailers are resorting to omnichannel retailing, similar to the use of omnichannel in insurance.

- The middle-class is driving the expansion of e-commerce, given the convenience and choice that online shopping offers. As competition intensifies, brands are expanding beyond e-commerce to "social commerce," i.e., engaging visually immersive social media experiences.

Trend 5: Increasing personal cybersecurity risks

Heightened digital activity has increased the susceptibility of middle-class consumers to cyber threats. This is reflected in Peak Re’s 2023 Consumer Survey, which shows that a whopping 65% of emerging Asia middle-class consumers have previously faced cybersecurity issues, such as hacking, phishing, and identity theft. As a result, there is high demand among the middle-class for insurance protection against cyberattacks.[12]

Along with the growth of digital consumption, there has been a proliferation of online payment options, digital wallets (e.g., PayTM, GrabPay), and other related services such as Buy Now, Pay Later (BNPL), that intensify the risk exposure of consumers.

Gig Economy Growth and Income Volatility

The rise of the gig economy has transformed many emerging Asian markets. It is estimated that the gig economy now involves over 200 million workers in China and 15 million in India[13], many in low-paying service roles, such as food delivery, or as professional freelancers. Many middle-class households rely on gig income to supplement earnings or as a temporary buffer in times of economic disruptions such as layoffs or hiring freezes.

Trend 6: The expanding gig economy’s financial vulnerability

Many workers in the gig economy lack formal protection, such as group insurance provided by employers, and typically rely on their own insurance. There is a need for flexible, on-demand insurance (e.g., professional liability, workers’ compensation). At the same time, gig workers face greater income volatility. Thus, they have a greater interest in income protection and disability coverage. Some start-up insurers are focusing on offering different insurance options to gig workers, particularly those in the middle-class.

There are opportunities here to partner with gig platforms (e.g. Grab, Gojek) to offer different insurance products catered to gig workers (including micro-coverage and subscription-based insurance for freelancers).

Conclusion

Emerging Asia’s burgeoning middle class is reshaping consumption, driven by expanding urban lifestyles, a rising gig economy, and digital habits. These shifts can redefine risk profiles and hence have significant implications for insurers.

While these long-term trends are poised to persist, it is crucial to consider them alongside short-term influences, such as from economic cycles, inflationary pressures and geopolitics, all of which can significantly affect consumer behaviour and spending decisions.

Insurers that are proactively developing flexible, digitally enabled, lifestyle-aligned products, designed to meet the evolving needs and expectations of this demographic, stand to benefit from the growth and complexity of this critical emerging market segment.

[1] Homi Kharas, The Rise of the Global Middle Class, 1 November 2023. Using a different definition, the Brookings Institution estimated that the middle class had surpassed half of the world's population in 2018.

[2] Homi Kharas, The Unprecedented Expansion of the Global Middle Class, An Update, Global Economy & Development at Brookings, Working Paper 100, February 2017.

[4] Urbanisation, United Nations Population Fund.

[5] McKinsey Global Institute: The trailblazing consumers in Asia propelling growth, 7 June, 2021

[6] Stress and the City: Mental Health in Urbanised vs. Rural Areas in Salzburg, Austria - PubMed, Urban vs. rural differences in psychiatric diagnoses, symptom severity, and functioning in a psychiatric sample - PMC

[7] (PDF) Rural-urban differences in health service utilisation in upper-middle and high-income countries: a scoping review

[8] Harvard Business School: Why Time Poverty Matters for Individuals, Organisations, and Nations, By: Laura Giurge, Ashley V. Whillans and Colin West

Disclaimer

Peak Re provides the information contained in this document for general information purposes only. No representation or guarantee is made as to the accuracy, completeness, reasonableness or suitability of this information or any other linked information presented, referenced or implied. All critical information should be independently verified and Peak Re accepts no responsibility or liability for any loss arising or which may arise from reliance on the information provided. All information and/or data contained in this document is provided as of the date of this document and is subject to change without notice. Neither Peak Re nor any of its affiliates accepts any responsibility or liability for any loss caused or occasioned to any person acting or refraining from acting on the basis of any statement, fact, text, graphic, figure or expression of belief contained in this document or communication.

All rights reserved. The information contained in this document is for your information only and no part of this document may be reproduced, stored or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of Peak Re. Any other information relating to this document, whether verbal, written or in any other form, given by Peak Re either before or after your receipt of this document shall be provided on the same basis as set out in this disclaimer. This document is not intended to constitute advice or recommendation, and should not be relied upon or treated as a substitute for advice or recommendation appropriate to any particular circumstances.

© 2025 Peak Reinsurance Company Limited.

Other Insights

Wed, 22 Apr 2026

| 16 mins

|

Frankie Chan

Tue, 24 Mar 2026

| 19 mins

|

Kritika Kashyap

Fri, 30 Jan 2026

| 18 mins

|

Kritika Kashyap

Mon, 27 Oct 2025

| 10 mins

|

Kritika Kashyap

Elevate Your Business

with Peak Re

with Peak Re